1. Introduction: The Silent Shift

For the "Sandwich Generation"—those adult children balancing the needs of their own kids with the care of aging parents—the realization that help is needed rarely arrives in a formal meeting. It usually happens during a holiday visit. You notice mom has lost weight, or dad is becoming "wobbly."

One of the most telling red flags isn't a medical diagnosis, but a fitted sheet. As Dwight Brown, owner of the national franchise Home Helpers, shared in our recent collaboration, when an 85-year-old struggles to wrestle a fitted sheet onto a mattress or carry a heavy laundry basket, they are one slip away from a life-altering crisis.

At Aragone & Advisors, we see how these moments collide with real estate and estate planning. This guide, featuring Dwight’s expert insights, is designed to help you move from reactive panic to a proactive transition strategy.

2. The 14-Day Medicare Window: A Strategic Head Start

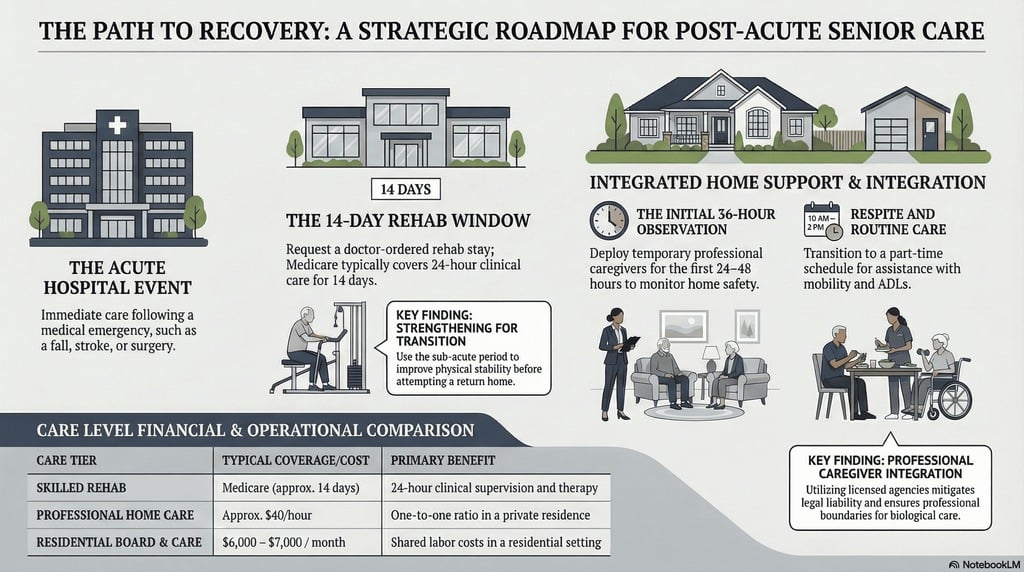

When a parent suffers an "acute event", a fall, a broken hip, or a stroke, the clock starts ticking on their recovery and your planning. Families often rush to bring a parent straight home from the hospital, but there is a more strategic path: the "Hospital Hotel."

Medicare typically covers approximately two weeks of stay at a rehabilitation facility following a hospitalization. This is a vital strategic window where your parent receives 24-hour care and professional physical therapy to regain strength. To secure this stay, you must advocate.

Talk to the doctor specifically about "fall risk."

"I always tell people: talk to the doctor. Say that mom or dad is potentially a fall risk, and they’ll keep you at a rehab for a couple of weeks... You get two weeks for mom and dad to get stronger and more capable, and then by the time they come home, hopefully, they’re able to stand up." — Dwight Brown

3. The "Hidden" Veteran Benefit (The 1% Utilization)

Perhaps the most overlooked financial tool for seniors is the VA’s caregiving support. Despite billions being set aside by Congress, the utilization rate for these benefits is under 1% because families simply don't know the rules.

There are three primary avenues, and as a strategist, I find the distinction between them critical:

- Caregiver Support for the Veteran: Professional in-home care for the veteran.

- Respite Care for the Spouse: Support to give a veteran a break from caregiving duties.

- Aid and Attendance Pension: A direct cash payment for care costs.

The Strategy Detail: Unlike many government programs, the first two (Caregiver Support and Respite) have no asset limits. You can qualify regardless of your net worth.

The Aid and Attendance pension, however, is income-limited, generally requiring assets below $120,000. For those with a trust or estate property, navigating these distinctions is essential to preserving family wealth.

4. The ADU Trend: Real Estate as a Care Strategy

In the current Orange County market, we are seeing a shift away from the traditional buy/sell model toward the "Multi-Generational Compound." Building an Accessory Dwelling Unit (ADU) or converting a garage is no longer just for "casitas"—it is an equity-preservation strategy.

This trend is accelerating due to a massive regulatory shift in California. In the past, cities like Yorba Linda required lots as large as 17,000 square feet to build a guest house. Today, those rules have been streamlined, allowing almost any homeowner to build.

This is a "double win." You provide your parents with proximity and dignity, avoiding the high cost of senior communities while investing in your own property value. Should your parents eventually require a higher level of facility care, that ADU becomes a luxury listing or high-end rental unit that generates the income needed to fund their next stage of life.

5. The Danger of "Under the Table" Care: A Financial Minefield

To save costs, many families hire private caregivers via Craigslist or neighborhood referrals.

This is a massive legal and financial risk. In California, an "under the table" hire is a $300,000+ lawsuit waiting to happen.

If a private caregiver is injured on your property or simply becomes disgruntled, they can sue the estate for years of unpaid overtime, minimum wage violations, and punitive damages.

One common nightmare occurs when a parent passes away and an unpaid caregiver sues the estate for hundreds of thousands in back pay and penalties that the family never budgeted for.

The National Franchise Advantage: By choosing an agency like Home Helpers, you benefit from a national franchise structure with rigorous checks and balances that "mom and pop" shops lack:

- Background Monitoring: Not just a one-time check; the agency is notified if an employee receives a DUI or criminal charge after being hired.

- Workers’ Comp & Liability: They carry the insurance, so a "slip and fall" doesn't become a claim against your parents’ home.

- Bonded and Licensed: Monitored through Social Services to prevent elder abuse.

- Financial Ethics: Professionals are strictly forbidden from discussing their own financial needs or managing a client’s checkbook.

6. The "Daughter vs. Caregiver" Dynamic: Preserving Relationships

The phenomenon of "Caregiver Stress" is real. Statistics show that the health of the family caregiver often declines faster than the person receiving care. This is fueled by the "role reversal"—parents often feel undignified having their children assist with biological needs like bathing or dressing.

Professional caregivers bring a level of training that family members simply don't have. For example, in cases of Alzheimer's or dementia, a parent may become aggressive or accusatory.

A daughter cannot "turn off" being a daughter and may take these attacks personally. A professional caregiver is trained to acknowledge, redirect, and remain detached, allowing the child to remain the "son or daughter" rather than the "enforcer."

"None of us want our kids taking care of our biological needs as we get older... by hiring a professional, you add that level of dignity. You get to remain the son or daughter, and we get to be the nurse." — Dwight Brown

7. Cost Comparison: Navigating the Financial Spectrum

Setting expectations early is the key to a successful transition. Whether you are planning a probate sale of a secondary property or managing a trust property, you must know the burn rate for care.

- Example Option

Estimated Monthly Cost

Level of Care

Board and Care : $6,000 - $7,000

Shared residential home; 24/7 divided care.

Memory Care Unit ~$20,000

Specialized facility for Dementia/Alzheimer's.

24/7 In-Home Agency~$30,000

One-on-one professional support in the home.

Strategy Tip: If 24/7 care is out of reach, consider the "Wellness Check" strategy. Agencies can often have caregivers stop by for 90-minute blocks on their way to other jobs.

This provides a professional "eye on the home" for tasks like medication checks or light tidying for a fraction of the cost. To fund these expenses, families often look to unlock equity through a reverse mortgage or a strategic probate sale.

8. Conclusion: The Power of Proactive Planning

The complexities of California real estate, probate, and elder care are difficult enough without the added weight of a medical emergency. Having an estate plan and Power of Attorney in place before a crisis occurs ensures that you dictate the choices, rather than the government or a hospital system.

Is your family's current plan based on strategy, or is it waiting for a medical emergency to dictate your choices?

- Watch: See the full story and more expert tips on the [Aragone & Associates YouTube Channel].

- Subscribe: Visit our Blog Main page to sign up for our newsletter and receive in your inbox our latest blogs articles.

- Listen: Catch the latest episodes of the Aragone & Advisors podcast on Spotify for deep dives into Orange County real estate strategy.

- Connect: Follow us for daily insights and probate advice on [Instagram], [Facebook], and [LinkedIn].

Let Aragone & Associates guide you through the process, helping to make the transition seamless. Call us at 949-415-4784 or email us at [email protected].

Disclaimer: We are not real estate attorneys, and the information provided should not be considered legal advice. We strongly recommend consulting with qualified legal counsel regarding your specific situation. If you do not currently have legal representation, feel free to reach out to us, and we can connect you with one of our trusted attorneys.

Check out this article next